Having personally been involved in Self Storage projects for 12 years, and DMWR having been working in the sector for over 20 years, the nature of storage has evolved significantly in that time. Not only is Self Storage more prominent as we go about our daily lives, it is also more understood by the general public. Usage and awareness of the industry is rising steadily to the point where now over 50% of people have a ‘good understanding’ of Self Storage’s services, according to the UK Self Storage Association’s (UKSSA) research.

This rise in awareness is hardly surprising when reviewing the UKSSA’s latest Annual Report: there are now over 3,100 Self Storage facilities in the UK, providing over 67 million sqft of space. Compared with 12 years ago, the amount of storage space was around half of what it is now (34.4 million sqft) and the number of storage facilities was less than a third of the number of those currently operating (approximately 975 facilities).

Self Storage buildings are typically located on prominent industrial sites along busy routes to maximise visibility and help raise awareness of their services for potential future customers. This isn’t an industry that benefits from impulse purchases (unless you can stretch the meaning to include purchases that contribute to cluttering our increasingly constrained living spaces), Self Storage tends to sit quietly in the background until needed – significant life events such as births, deaths, marriages and divorces often give reason for new customers to consider means of storing their possessions. At present, three-quarters of Self Storage customers in the UK are domestic users, a percentage that is slowly increasing as small properties are overwhelmed by our belongings and while more of us are accustomed to spending time working from home, repurposing spaces into offices.

This large increase in the number of Self Storage facilities has been driven up by a significant increase in Operators. It is likely that there are around 1,500 operators running the 3,100+ facilities, with the 5 largest accounting for around two fifths of the total storage space. Approximately one third of the storage sites are containers only operations, a much less impactful low-rise solution for suburban and rural storage sites. The remaining sites are ‘built’ stores which are often repurposed buildings, but for the top end of the market are bespoke new build facilities in urban locations. The increased pool of operators has resulted not only in increased competition for prime industrial sites that come to the market but has also driven up the land prices. The established operators, and those with ambition and deep pockets, are now starting to look beyond the traditional industrial sites, seeking locations in commercial and residential districts.

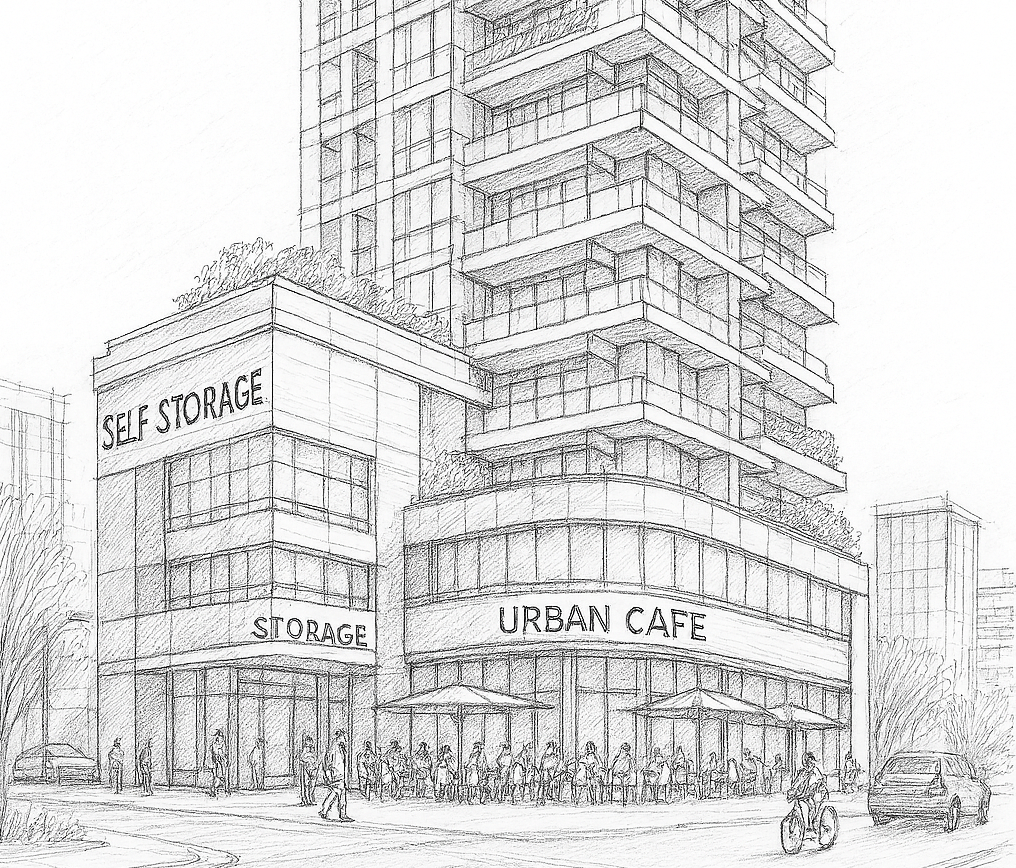

In the major urban centres, storage operators are now eyeing the same sites as residential, PBSA and hotel operators. These are locations which are more central, have more townscape constraints and require considerably more time, money and effort to nurture a successful Planning outcome.

The reason for Self Storage moving outside of its perceived lane is simple: it is maturing as a product and sector. Operators have the tools and resources required to compete for higher profile sites and with high calibre development teams and can navigate both Planning and operational hurdles to deliver a new generation of Self Storage buildings. But with higher profile sites comes enhanced levels of scrutiny, not just from Planning Authorities, but also from the general public. Colourful clad boxes wouldn’t and shouldn’t be acceptable in anything except the most industrial of locations. Sites in more built-up areas which are overlooked by residential and other sensitive receptors need to treated with due respect and designed accordingly. The implications are simple – storage design has had to grow up. Large swathes of brightly coloured metal cladding panels in our urban centres will not get the support of Planning Authorities, who are looking for more nuanced an articulated facades in prominent positions on their high streets. The colours used are becoming more muted and the palette of materials is more mature, echoing the facades of modern residential and commercial buildings.

But Self Storage isn’t done yet. The appetite for storage is growing, fuelled by Boomers and Gen X, now Gen Z are in the crosshairs as their migration to micro city living accommodation (units can be as small as 18sqm / less than 200sqft) should help maintain demand. Storage is all around us and people are no longer afraid to use it, with women now accounting for over 41% of customers. Facilities are evolving beyond the utilitarian masculine environments of the past, with more modern operators providing attractive customer facing areas created by interior designers which include working zones and kitchenettes to allow customers to dwell, check emails and make calls. This approach is very much deliberate, making your Self Storage trip less of a chore and more a lifestyle choice.

The next wave of Self Storage stores will soon be in an urban centre near you. Following how food retailers have expanded their reach with convenience outlets, smaller storage sites will also start to appear in vacant retail units, offices and disused underground car parks – filing the gaps between larger facilities, appealing to those within walking distance. There will also be choice. Whether an individual’s storage needs will be driven by price, ESG, branding or how good the coffee is, operators are starting to tailor their product to appeal to certain demographics. Both exterior and interior design have an important role to play in defining image – as does branding, online presence and advertising to create a joined-up approach to brand identity. Like food retail, phones or cars, price point and image will dictate who you give your business to.

So, the future of Self Storage – as storage becomes ever more part of our daily lives will become more integrated into our urban landscapes and routines. There is no reason why large scale mixed-use developments won’t have Self Storage components to them. We may even get to a point where Local Authorities require Self Storage to be part of residential-led developments as space standards in unitised accommodation are so meagre. Storage units in this scenario would effectively become a remote garage or loft: your stored goods accessible without the need to remove your slippers.

Whether Self Storage develops into mixed use urban blocks, small satellite unit infills, refurbished existing buildings or all of the above, DMWR Architects is well placed to continue to push the boundaries and deliver planning permissions and buildings in this burgeoning sector. Our experience and knowledge within the Self Storage sector is extensive, and we have been involved in new build and refurbishment schemes of all sizes across the country.

By Jeff Stokes, Director of DMWR Architects